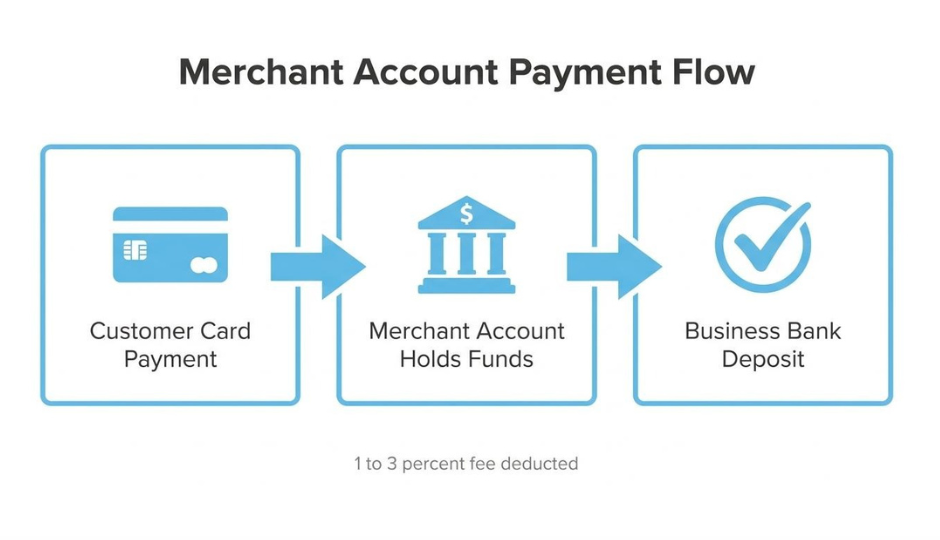

A merchant account is a specialized bank-held account that temporarily receives card payment funds on behalf of a business before depositing them into its operating bank account. It serves as the financial intermediary that makes accepting credit and debit cards possible, handling authorization, clearing, and settlement for every transaction.

This guide covers how merchant accounts function within the card transaction lifecycle, the account types and key players involved in processing, the layered fee structures and pricing models that determine cost, the application and underwriting process including reserves, and the compliance and channel considerations that affect merchants selling online and in-store.

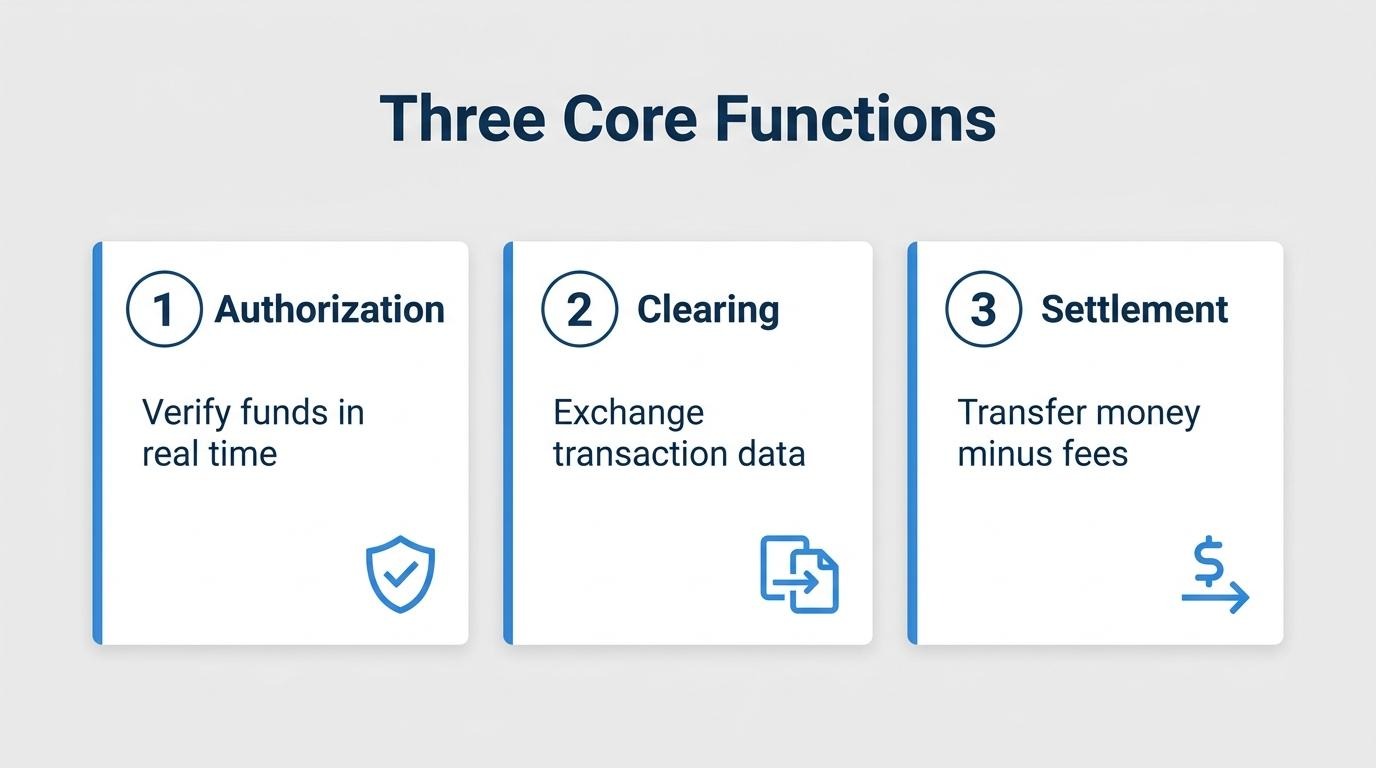

Each card transaction moves through three sequential stages: authorization verifies the cardholder's funds in real time, clearing exchanges transaction data between banks, and settlement transfers money (minus fees) into the merchant's account. The merchant discount rate deducted during this process typically falls between 1% and 3% per transaction, making the mechanics of each stage directly relevant to cash flow.

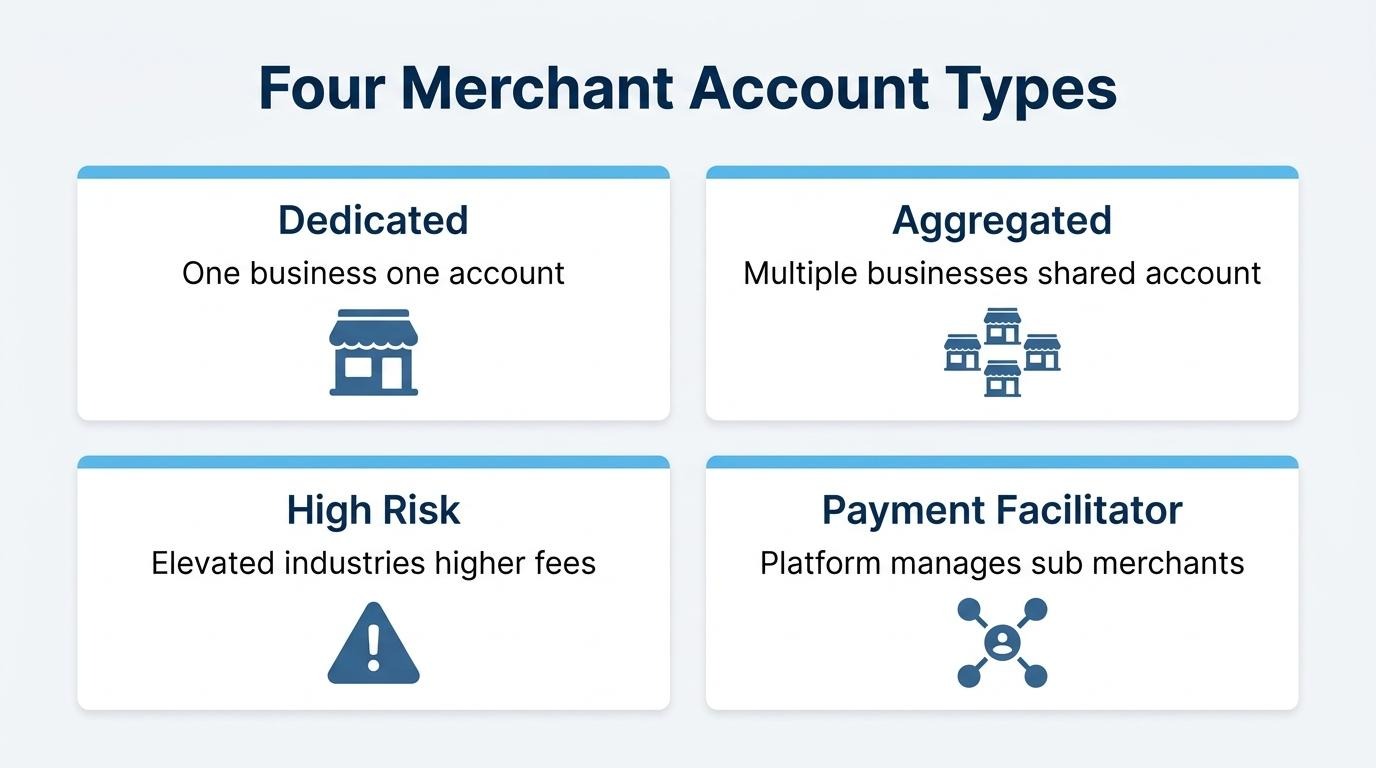

Merchant accounts come in dedicated, aggregated, high-risk, and payment facilitator sub-merchant structures, each carrying different underwriting requirements, fee terms, and levels of processing control. Five distinct entities participate in every transaction: the acquiring bank, payment processor, card network, issuing bank, and payment gateway.

Cost layers stack from non-negotiable interchange and assessment fees through negotiable processor markups, chargeback penalties, and monthly minimums. Pricing models such as interchange-plus, flat-rate, tiered, and subscription each structure these costs differently, with transparency varying significantly between them.

Acquirers evaluate business risk through underwriting criteria spanning industry classification, chargeback history, and processing volume; elevated risk triggers reserve requirements. PCI DSS v4.0.1 compliance governs how every merchant protects cardholder data. For businesses selling across both online and physical channels, consolidating payment and customer data into a single system eliminates reconciliation gaps and maintains margin visibility as fee structures grow more complex.

A merchant account serves as the intermediary holding account that receives, processes, and settles card payment funds before they reach a business's operating bank account. It handles three core functions: authorizing transactions, clearing payment data between banks, and settling funds after deducting applicable fees.

A merchant account authorizes each card transaction by communicating with the issuing bank in real time to verify the cardholder's available credit or funds. According to guidelines cited by the International Air Transport Association, a regular authorization request is generally valid for 7 days; if the approval code expires, the transaction is considered unauthorized and can be rejected by the card issuer without a possibility of remediation. This time sensitivity is why batching and settlement timing matter so much for merchants managing cash flow.

Once authorized, the merchant account facilitates clearing and settlement. As outlined by the Federal Reserve Bank of Philadelphia, clearing involves the transfer of transaction information between parties, while settlement is the exchange of monetary value between the issuing bank (the cardholder's bank) and the acquiring bank (the merchant's bank). The merchant discount rate deducted during settlement typically ranges from 1% to 3% per transaction, with credit card interchange rates for U.S. retail transactions falling between 1.5% and 2.5% for non-premium cards as of 2024.

The merchant account also absorbs chargeback liability. Research from the Federal Reserve Bank of Kansas City found that Visa and MasterCard chargebacks average 1.6 basis points of sales by number and 6.5 basis points by value, with 70 to 80 percent resolved as merchant liability. This means the merchant account is not just a pass-through for funds; it carries real financial exposure that makes proper transaction management essential.

For merchants processing significant volume, understanding these mechanics is not optional. Every expired authorization, delayed batch, or uncontested chargeback represents money lost, and the merchant account sits at the center of each of those outcomes. The step-by-step processing flow that follows breaks down exactly how authorization, clearing, and settlement work in sequence.

Credit card payment processing works through three sequential stages: authorization, clearing, and settlement. Each stage involves distinct data exchanges between the merchant, acquiring bank, card network, and issuing bank.

The authorization stage is when the merchant's system sends a real-time request to verify that the cardholder's account can cover the transaction. After a customer taps, swipes, or enters card details online, the payment terminal or gateway transmits transaction data to the acquiring bank. The acquirer routes this request through the card network (Visa, Mastercard, etc.) to the issuing bank, which checks the account for sufficient credit, fraud flags, and card validity. Within seconds, the issuer returns an approval or decline code back through the same chain. An approved authorization places a temporary hold on the cardholder's funds but does not yet move money.

The clearing stage is when transaction details are formally exchanged between the acquiring bank and the issuing bank to prepare for fund transfer. According to the Federal Reserve Bank of Philadelphia, clearing involves the transfer of information pertaining to card-based transactions, while settlement is the separate exchange of monetary value between issuers and acquirers. During clearing, the merchant submits a batch of authorized transactions, typically at the end of each business day. The card network calculates interchange fees owed and reconciles the data between both banks. This intermediate step confirms exact amounts, applies applicable fee deductions, and flags any discrepancies before money moves.

The settlement stage is when funds are actually transferred from the issuing bank to the acquiring bank and then deposited into the merchant account. Once clearing reconciliation is complete, the card network facilitates the net financial exchange. The issuer sends the transaction amount, minus interchange and assessment fees, to the acquirer. The acquirer then deducts its processor markup and deposits the remaining balance into the merchant's account, typically within one to three business days.

Given that U.S. cards generated $11.903 trillion in purchase volume in 2024 according to the Nilson Report, even small inefficiencies at the settlement stage compound significantly at scale. For merchants processing high volumes across multiple channels, understanding where each fee is deducted during settlement is essential for accurate cash flow forecasting.

The types of merchant accounts are dedicated, aggregated, high-risk, and payment facilitator sub-merchant accounts. Each type differs in underwriting, risk exposure, and how transaction funds are held before reaching the business.

A dedicated merchant account is a standalone account assigned exclusively to one business by an acquiring bank. The merchant undergoes individual underwriting, receives a unique merchant identification number (MID), and holds its own settlement account. This structure gives businesses direct control over transaction processing, deposit timing, and chargeback management.

Dedicated accounts suit established businesses with consistent sales volume, since the individual underwriting process evaluates creditworthiness, processing history, and industry risk before approval. According to Paycron, navigating merchant account options requires small businesses in the U.S. to weigh approval complexity against the greater processing flexibility a dedicated account provides. For brands processing significant monthly volume, the predictability of a dedicated MID often justifies the longer setup timeline.

An aggregated merchant account pools multiple businesses under a single master merchant account managed by a payment service provider (PSP). Instead of individual underwriting, the PSP onboards sub-merchants quickly under its own MID, handling compliance and settlement on their behalf.

Key characteristics of aggregated accounts include:

This model works well for newer or lower-volume businesses that prioritize speed over processing independence. The trade-off is less control over fund holds, reserve requirements, and dispute handling compared to a dedicated account.

A high-risk merchant account is a dedicated account structured for businesses in industries that acquiring banks classify as elevated risk. Categories typically flagged as high-risk include subscription billing, travel services, nutraceuticals, and adult entertainment.

High-risk accounts carry distinct terms:

Acquirers justify these terms because high-risk industries historically generate more chargebacks and fraud exposure. For merchants in these verticals, securing a high-risk account is often the only path to accepting card payments directly.

A payment facilitator (PayFac) sub-merchant account is an account created when a payment facilitator registers a business under its own master merchant relationship with an acquiring bank. The PayFac handles underwriting, onboarding, compliance, and fund disbursement for its sub-merchants.

This model differs from simple aggregation because the PayFac assumes greater regulatory responsibility, including KYC verification and transaction monitoring for each sub-merchant. Platforms operating as PayFacs can customize the checkout experience, set pricing, and manage disputes directly, giving sub-merchants a more integrated payment flow than a standard aggregated setup provides.

Understanding these account structures helps clarify the fee models and provider relationships covered next.

The key players in merchant account processing are the acquiring bank, the payment processor, the card network, the issuing bank, and the payment gateway. Each handles a distinct function within the transaction flow.

The acquiring bank plays the role of the merchant's financial sponsor in the card payment ecosystem. It underwrites and holds the merchant account, assumes liability for transactions the merchant processes, and receives settled funds from the card network on the merchant's behalf. When a chargeback occurs, the acquiring bank is responsible for debiting the merchant and returning funds to the cardholder's issuer. This financial liability is why acquirers evaluate business risk carefully before approval. According to the Nilson Report, U.S. card purchase volume reached $11.903 trillion in 2024, underscoring the scale of funds acquirers manage daily.

The payment processor plays the role of the technical intermediary that routes transaction data between all other parties. It captures the cardholder's payment information, formats authorization requests, and transmits them to the card network. Once approved, the processor sends the confirmation back to the merchant's point-of-sale terminal or online checkout. During clearing, it batches completed transactions and submits them for settlement. Many merchants interact with their processor more than any other entity in the chain, since the processor typically provides reporting dashboards, manages billing, and serves as the primary support contact for day-to-day transaction issues.

The card network plays the role of the central routing and rule-setting authority for card transactions. Visa, Mastercard, American Express, and Discover each operate proprietary networks that connect acquiring banks to issuing banks. These networks set interchange fee schedules, define dispute resolution timelines, and enforce compliance standards that all participants must follow. They do not issue cards or hold merchant accounts directly; instead, they function as the infrastructure layer that makes interoperability possible. For merchants, the card network's rules determine data security requirements that shape the overall cost of acceptance.

The issuing bank plays the role of the cardholder's financial institution. It issues credit or debit cards, extends credit lines, and approves or declines individual transactions based on the cardholder's available balance, fraud signals, and account standing. When a transaction is authorized, the issuing bank places a hold on the cardholder's funds. During settlement, it transfers the transaction amount, minus interchange fees, to the acquiring bank through the card network. The issuer also initiates chargebacks when cardholders dispute charges, making it the first point of contact on the consumer side of any payment dispute.

The payment gateway plays the role of the secure data bridge between the merchant's checkout interface and the payment processor. It encrypts sensitive card data at the point of capture, whether from an online form, mobile app, or in-store terminal, then transmits that encrypted data to the processor for authorization. Gateways also handle tokenization, replacing card numbers with non-sensitive tokens for recurring billing and stored-card functionality. While often confused with the processor itself, the gateway is specifically the encryption and transmission layer. Understanding each player's role clarifies which fees appear on a merchant statement and where to direct questions about costs.

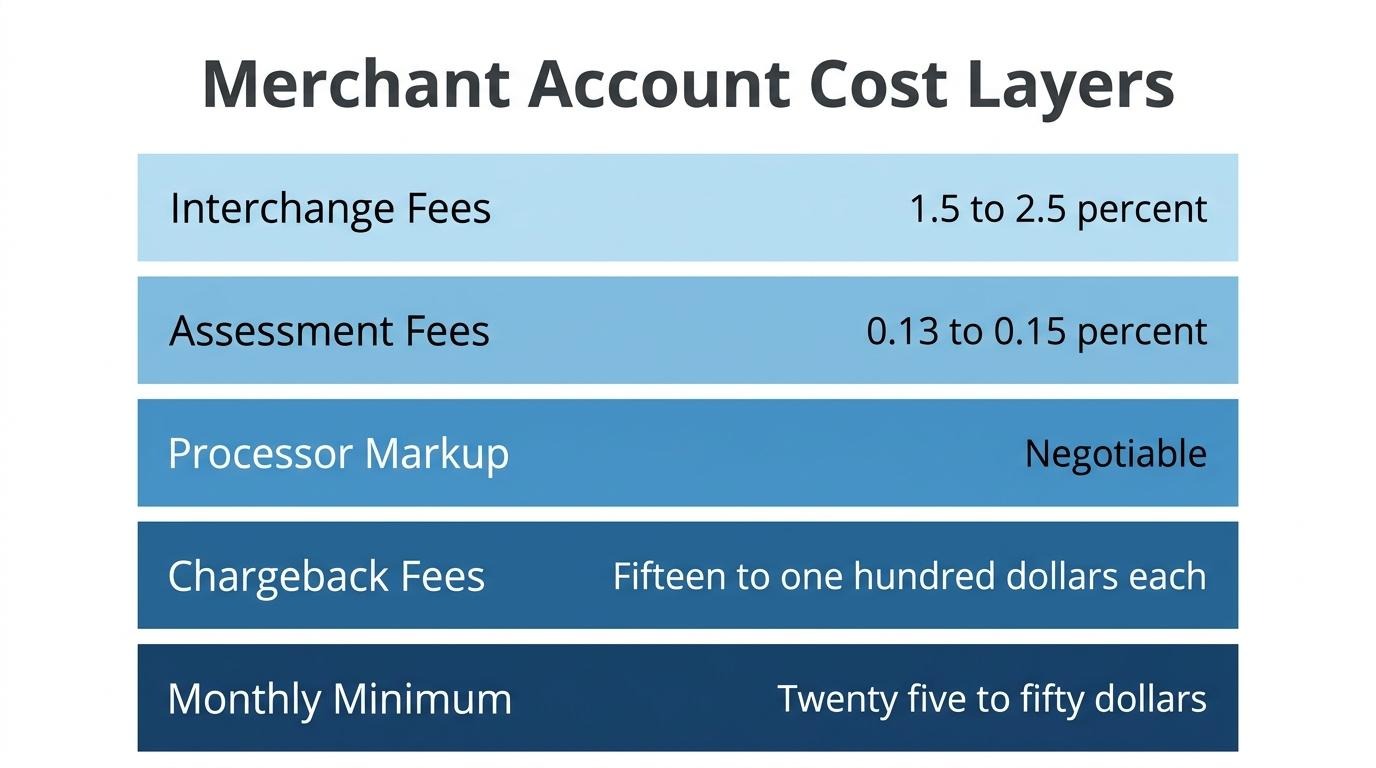

A merchant account cost includes interchange fees, assessment fees, processor markups, chargeback fees, and monthly minimums. The following sub-sections break down each cost layer.

Interchange fees are transaction-based charges set by card networks like Visa and Mastercard, paid by the acquiring bank to the issuing bank each time a cardholder makes a purchase. These fees compensate issuers for credit risk, fraud exposure, and the cost of funding the transaction float.

Rates vary by card type, transaction method, and merchant category. According to a 2024 report from the Federal Reserve Bank of Kansas City, credit card interchange rates for retail transactions in the United States typically range between 1.5% and 2.5% for non-premium cards, with higher rates applied to premium or rewards-based cards. Debit interchange for covered issuers is capped under Regulation II. Interchange is non-negotiable; it passes through to every merchant regardless of processor.

Assessment fees are small percentage-based charges collected by card networks (Visa, Mastercard, American Express, Discover) on every transaction processed through their rails. These fees fund network operations, brand maintenance, and infrastructure.

Unlike interchange, assessment fees go directly to the card network rather than the issuing bank. They typically range from 0.13% to 0.15% of transaction volume, though exact rates vary by network and card type. Assessment fees apply uniformly across all merchants on a given network. Because they are set by the networks themselves, merchants cannot negotiate them. They appear as a separate line item on processing statements, distinct from both interchange and processor markup.

Processor markup fees are the charges a payment processor adds on top of interchange and assessment fees to cover its own services. This markup is the only negotiable component in the merchant account fee stack.

Markups take different forms depending on the pricing model. Under interchange-plus, a processor might add a fixed per-transaction fee plus a small percentage. Flat-rate processors bundle everything into one rate. The markup covers transaction routing, reporting, customer support, and fraud tools. For merchants processing significant volume, even small differences in processor markup compound quickly. This is where comparing providers yields the most direct savings.

Chargeback and incidental fees are penalty-based charges merchants incur when transactions are disputed, reversed, or require special handling. A chargeback fee, typically $20 to $100 per occurrence, covers the administrative cost of processing the dispute through the card network.

Incidental fees include charges for batch processing, PCI non-compliance, account setup, early termination, and retrieval requests. These costs vary widely by processor and contract terms. Merchants with high dispute ratios face compounding costs; elevated chargeback rates can trigger monitoring programs with additional fines. Proactive fraud screening and clear return policies reduce chargeback exposure more effectively than reactive dispute management.

A monthly minimum is a guaranteed floor payment a merchant owes to the processor each billing cycle, regardless of actual processing volume. If total processing fees fall below the minimum, the merchant pays the difference.

A statement fee, typically $5 to $15 per month, covers the cost of generating and delivering monthly processing reports. Some processors bundle both charges; others list them separately. These fixed costs matter most for low-volume merchants, where they represent a larger percentage of revenue. High-volume businesses usually exceed the monthly minimum through transaction fees alone, making it functionally irrelevant.

Understanding each cost layer positions merchants to evaluate pricing models, which the next section covers in detail.

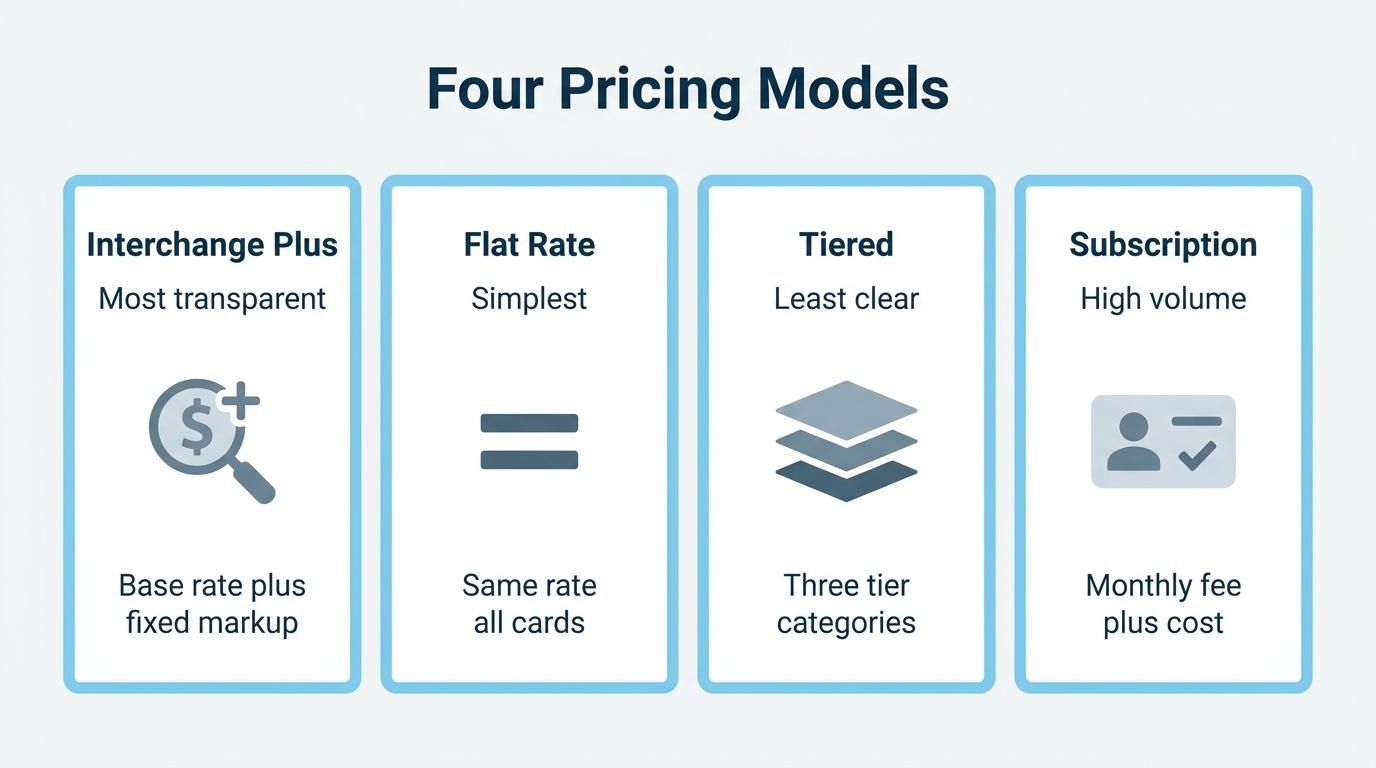

The common merchant account pricing models are interchange-plus, flat-rate, tiered, and subscription-based. Each structures processor costs differently, affecting how predictable and transparent monthly statements become.

Interchange-plus pricing separates the base interchange fee from the processor's fixed markup. Every transaction shows two components:

This model offers the highest transparency because merchants can see exactly what goes to the card network and what goes to the processor. For scaling brands processing significant volume, interchange-plus typically yields the lowest effective rate. It does require comfort reading itemized statements, though, since line items vary month to month.

Flat-rate pricing charges a single, uniform percentage on every transaction regardless of card type or network. A merchant pays the same rate whether the customer uses a basic debit card or a premium rewards credit card.

This simplicity makes flat-rate attractive for lower-volume businesses or those prioritizing predictable costs. The trade-off is overpayment on cheaper card types; debit transactions that carry low interchange still get charged the full flat rate. As monthly volume grows, the gap between what a merchant pays under flat-rate versus interchange-plus widens considerably. Businesses processing above roughly $10,000–$15,000 monthly often find the simplicity premium no longer justifies the cost.

Tiered pricing groups transactions into categories, typically labeled qualified, mid-qualified, and non-qualified, each carrying a different rate. The processor assigns each transaction to a tier based on criteria like card type, whether the card was present, and how the transaction was entered.

This model is the least transparent of the four. Processors control which transactions fall into which tier, and merchants rarely know the classification rules in advance. A transaction that seems routine can land in the most expensive tier without clear explanation. In some payment models, merchants may even need to deposit funds upfront in a trust account to mitigate settlement risks, according to a World Bank whitepaper on digital financial services. For most merchants, tiered pricing makes cost optimization nearly impossible.

Subscription or membership pricing charges a fixed monthly fee in exchange for direct-cost interchange rates with zero percentage markup from the processor. Instead of adding a margin to each transaction, the processor collects revenue through the flat membership fee plus a small per-transaction cent fee.

This structure benefits high-volume merchants most. The monthly fee stays constant whether a business processes $50,000 or $500,000, so the effective per-transaction cost drops as volume increases. Lower-volume merchants may find the fixed fee disproportionate relative to their savings on interchange passthrough.

Choosing the right pricing model depends on transaction volume, average order value, and how much statement transparency a business needs to manage margins effectively.

You apply for and get approved for a merchant account by submitting a formal application to an acquiring bank or payment processor, which then evaluates your business through an underwriting review. The process covers documentation, risk assessment, and contract negotiation.

To complete a merchant account application, most acquirers require the following documentation:

After submission, the acquirer's underwriting team assesses risk based on industry type, processing volume, chargeback history, and the owner's personal credit profile. Businesses in categories like travel, nutraceuticals, or subscription billing often face additional scrutiny due to higher historical chargeback rates. Approval timelines range from 24 hours for low-risk profiles to several weeks for high-risk applicants requiring manual review.

For merchants selling across both online and in-store channels, having consistent business data across all touchpoints strengthens the application; acquirers look for operational stability and clear transaction records. Understanding what underwriting criteria acquirers evaluate in detail helps merchants prepare stronger applications from the start.

Acquiring banks evaluate underwriting criteria that measure a merchant's financial stability, transaction risk profile, and likelihood of generating chargebacks or fraud. The criteria span business history, industry classification, and processing volume projections.

The acquiring bank begins its assessment before a merchant account is approved, and the depth of review scales with the perceived risk level of the business. Merchants in industries with higher chargeback rates or longer fulfillment windows face more scrutiny. Understanding these criteria helps merchants prepare stronger applications and avoid delays.

Key underwriting criteria include:

According to the International Finance Corporation, merchant account underwriting involves assessing business risk, and acquirers may require reserves such as a rolling reserve (a percentage of daily sales held for a set period) or a capped reserve (funds held until a specific threshold is reached). These reserve structures protect the acquirer if chargebacks or refunds exceed the merchant's available balance.

For merchants processing across both online and in-store channels, underwriting often examines whether transaction data consolidates into a single risk view or fragments across disconnected systems. A clean, unified processing history simplifies the acquirer's evaluation and can result in more favorable terms. With underwriting criteria established, the next consideration is how reserves function once an account is approved.

A merchant account reserve is a portion of a merchant's processed sales that an acquiring bank holds back to cover potential chargebacks, refunds, or financial losses. Reserves are required when the acquirer's underwriting assessment determines that a business poses elevated settlement risk.

According to the International Finance Corporation's handbook on merchant payments, acquirers may require reserves such as a rolling reserve, where a percentage of daily sales is held for a set period, or a capped reserve, where funds are held until a specific threshold is reached. A third type, the upfront reserve, requires a lump-sum deposit before processing begins.

Acquirers typically impose reserves on businesses that meet one or more of these risk criteria:

Rolling reserves are the most common structure for mid-risk merchants because they release automatically after the holding period expires, typically 90 to 180 days. Capped reserves stop accumulating once the target amount is met, which makes them more predictable for cash flow planning. For most scaling brands, understanding which reserve type applies helps avoid surprises when negotiating processor terms.

With reserve requirements clarified, the next step is understanding how chargebacks directly impact a merchant account.

Chargebacks affect a merchant account by reversing completed transactions, triggering fees, and increasing the merchant's risk profile with the acquiring bank. The financial and operational consequences compound quickly when dispute rates climb.

When a cardholder disputes a charge, the issuing bank pulls the funds from the merchant account and returns them to the customer. According to a Federal Reserve Bank of Kansas City study, chargebacks received by Visa and MasterCard merchants average 1.6 basis points of sales by number and 6.5 basis points by value, with approximately 70 to 80 percent resolved as merchant liability. That resolution ratio means most disputes end with the merchant absorbing the loss.

Each chargeback carries a fee, typically $20 to $100 per incident, on top of the reversed transaction amount. The merchant also loses the product or service already delivered, the original processing fees, and any shipping costs. These layered losses make even a modest chargeback rate expensive at scale.

Card networks like Visa and Mastercard monitor chargeback ratios closely. Merchants that exceed threshold levels, generally around 1% of transactions, enter monitoring programs that impose additional fines, mandatory remediation plans, and higher processing rates. Sustained violations can lead to account termination by the acquiring bank, effectively cutting off a merchant's ability to accept card payments.

The dispute management process itself drains resources. As Fatemah Nikayin, co-founder of Rivero, describes it, the process "is very manual and costly," requiring large teams to receive, process, and submit requests to the payment networks. For growing brands, this operational burden diverts staff from revenue-generating work toward paperwork and evidence gathering.

Proactive chargeback prevention, including clear billing descriptors, responsive customer service, and real-time fraud detection, is far less expensive than fighting disputes after they occur. Merchants who treat chargebacks as a lagging indicator rather than building upstream defenses tend to face escalating costs that erode margins over time.

With chargeback risks understood, maintaining PCI DSS compliance adds another layer of merchant account protection.

PCI DSS compliance isn’t optional–it’s a set of security standards that every merchant handling card payments is legally and contractually obligated to follow to protect cardholder data. It matters because non-compliance exposes businesses to data breaches, financial penalties, and loss of the ability to accept card payments. The standard governs how merchants store, process, and transmit sensitive payment information.

The PCI Security Standards Council maintains the framework. All businesses that accept, process, or store cardholder data are required to comply, regardless of transaction volume. Compliance levels vary based on the number of annual card transactions a merchant processes, with Level 1 applying to the highest-volume merchants and Level 4 covering the smallest.

PCI DSS v4.0.1 is the current active version of the standard. According to the PCI Security Standards Council, PCI DSS v4.0 was retired on December 31, 2024, after which v4.0.1 became the only supported version. These latest versions introduce greater flexibility through customized implementation, allowing merchants to meet requirements based on their specific infrastructure and security environment rather than following a rigid, one-size-fits-all checklist.

Core requirements span six categories:

Failing to meet these requirements carries real consequences. Card networks can levy fines against acquiring banks, which pass those costs to non-compliant merchants. Repeated violations can result in placement on the MATCH list (Member Alert to Control High-risk Merchants), effectively blacklisting the business from obtaining a merchant account.

For merchants managing payments across both online and in-store channels, PCI scope becomes more complex because each environment introduces distinct data touchpoints that must be secured independently. Understanding this compliance framework is essential before evaluating how merchant accounts differ from payment gateways.

A merchant account differs from a payment gateway in function, ownership, and where each sits in the transaction flow. The merchant account holds funds; the gateway transmits data. Below are the core distinctions.

A merchant account is a bank-held account that temporarily receives card transaction funds after settlement. The acquiring bank or payment processor owns and underwrites this account on the merchant's behalf. Its primary role is financial: holding, reconciling, and releasing funds to the merchant's business bank account.

A payment gateway is a technology layer that encrypts and routes transaction data between the merchant's checkout and the payment processor. It performs no fund-holding function. Instead, it acts as a secure digital bridge, comparable to a physical card terminal but for online and omnichannel environments.

Key functional differences include:

According to Paycron, "What is the difference between a payment gateway and a merchant account?" ranks among the most common queries businesses ask when evaluating card payment infrastructure.

For most merchants, both components are necessary. Some providers bundle them into a single service, while others require separate agreements for each. Understanding where each piece fits helps merchants evaluate costs, compliance obligations, and provider contracts more accurately.

You choose the right merchant account provider by evaluating pricing transparency, contract terms, integration capabilities, support quality, and risk management policies. The factors below cover what matters most during selection.

Pricing structure clarity. Providers offering interchange-plus pricing disclose exactly what goes to the card network and what the processor keeps. Flat-rate and tiered models can obscure true costs, especially as transaction volume grows. Request a full fee schedule before signing, including chargeback fees, PCI compliance fees, monthly minimums, and early termination penalties.

Contract length and exit terms. Some providers lock merchants into multi-year agreements with liquidated damages clauses. Others offer month-to-month terms. For scaling brands processing higher volumes, a longer contract may secure lower rates, but the exit cost must justify the commitment.

Integration with existing systems. The provider's payment gateway, POS compatibility, and API flexibility determine how smoothly transactions flow into accounting, inventory, and CRM systems. Disconnected tools create reconciliation headaches that compound at scale.

Chargeback and dispute support. Providers differ significantly in how they handle disputes. Some offer real-time chargeback alerts, automated evidence submission, and dedicated dispute analysts. Others leave merchants to navigate the process alone. Given that roughly 70 to 80 percent of chargebacks resolve as merchant liability, according to a Federal Reserve Bank of Kansas City study on Visa and MasterCard transactions, proactive dispute tools directly protect revenue.

Underwriting transparency and reserve policies. Providers should clearly explain their underwriting criteria, expected approval timelines, and whether rolling or capped reserves apply. Surprises in held funds disrupt cash flow, particularly for seasonal or high-ticket businesses.

Security and compliance support. A provider that simplifies PCI DSS compliance through hosted payment pages, tokenization, and regular vulnerability scanning reduces the merchant's compliance burden. This matters more as PCI DSS v4.0.1 introduces stricter requirements.

Scalability across channels. Merchants selling both online and in-store need a provider whose payment infrastructure supports unified reporting and consistent customer data across channels. Evaluating this upfront prevents costly migrations later.

For merchants already managing complexity across multiple tools, the selection process is also an opportunity to assess whether consolidating payment processing within a broader commerce platform reduces operational overhead compared to maintaining separate provider relationships.

Selling across both online and in-store channels multiplies payment complexity, because each channel carries distinct authorization rules, fee structures, and data flows. Unifying payment and customer data into one system reduces this complexity significantly.

Payment data and customer data gain real-time accuracy and consistency when they live in one system instead of separate tools. Unified commerce connects all back-end systems, including ERP, CRM, and POS, with customer-facing channels in a single platform, ensuring consistent data across every touchpoint, according to IMRG.

Separate tools create specific operational problems:

Starting April 2025, Visa implemented a 0.05% participation fee on Commercial Enhanced Data Program transactions that include Level 2 or Level 3 data. Tracking these granular fee changes across siloed tools compounds operational overhead. A single data layer eliminates duplicate records and gives operators one view of costs, customers, and disputes across channels. For brands processing meaningful volume in both online and physical retail, consolidation is not just convenient; it is the only way to maintain margin visibility as fee structures grow more layered.

The key takeaways about merchant accounts and card payments center on understanding the infrastructure, costs, and operational decisions that determine how efficiently a business accepts cards.

According to Don Apgar, Director of Merchant Payments at Javelin Strategy & Research, the integration of Buy Now, Pay Later for merchants shows how the payment business "has come full circle" in its evolution. This signals that merchant account infrastructure must now accommodate installment methods alongside traditional card rails. With U.S. credit card purchase volume reaching approximately $6.1 trillion in 2024, the scale of card-based commerce demands that operators treat payment infrastructure as a strategic function, not a back-office afterthought.